2 No-Brainer Payment Network Stocks to Buy With $1,000 Right Now

Sometimes, getting too cute with buying great stocks can cost you money. Payment network companies Visa (NYSE: V) and Mastercard (NYSE: MA) dominate the global payments space. Their networks power an estimated 90% of all payment processing volume outside of China, which uses a state-run network.

These companies have generated remarkable wealth for shareholders despite always commanding an expensive stock valuation. Today, both companies trade at reasonable or "fair" prices, which makes them no-brainer buys.

This Fool will outline what you can expect from the dynamic duo and why investors should consider investing the $1,000 it takes to own at least one share of each business.

Why Visa and Mastercard are always expensive

These two payment network companies are almost always trading at lofty valuations. In fact, Visa and Mastercard have averaged a price-to-earnings (P/E) ratio of 34 and 37, respectively, over the past decade. For reference, the S&P 500's P/E ratio is currently 24. Yet, had you bought a decade ago and held on, you would have done very well for yourself.

Both stocks have outperformed the broader market; Visa is up 463%, and Mastercard is up 555%, compared to the S&P 500's 235% gain.

Visa and Mastercard's dominance of payment networks has enabled them to enjoy a massive global shift from cash to debit, credit, and digital payments. Both companies act like toll booths; they receive a small fee for every payment that uses their network. Their market share virtually squeezes competitors out of the picture.

Since the payment networks require little maintenance to operate, both Visa and Mastercard have become remarkably profitable with size. Visa converts a staggering $0.60 of every revenue dollar to free cash flow, while Mastercard converts $0.43 of every revenue dollar.

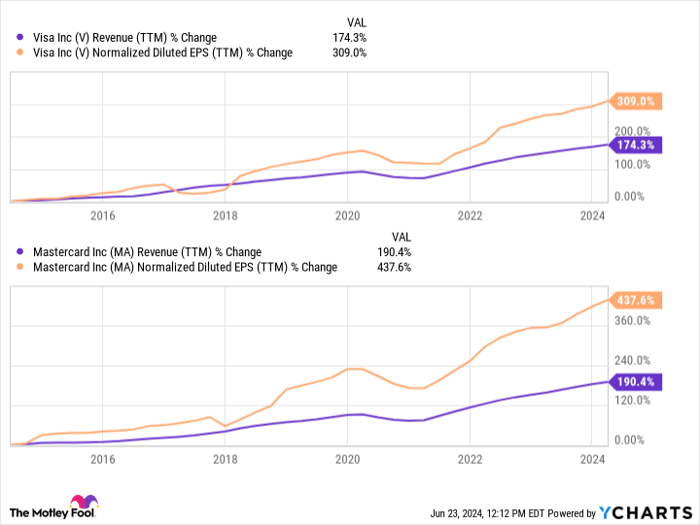

So, not only are Visa and Mastercard growing organically as people worldwide drop cash for debit, credit, and digital payments, but they also use their tremendous cash flow to repurchase shares to boost earnings growth further. Just look at how much earnings have grown compared to revenue. That's why both stocks have commanded premium valuations:

V Revenue (TTM)

Can these stocks continue justifying their steep price tags?

The most significant risk facing investors is that these stocks lose their premium valuation, which could significantly hurt the share price. Falling from a P/E ratio of 35 to, say, 25 would require roughly a 30% drop. The biggest factor working against these companies is becoming their size. Today, Visa and Mastercard's respective market caps are $550 billion and $422 billion. It naturally gets harder to maintain growth percentages as the numbers get larger.

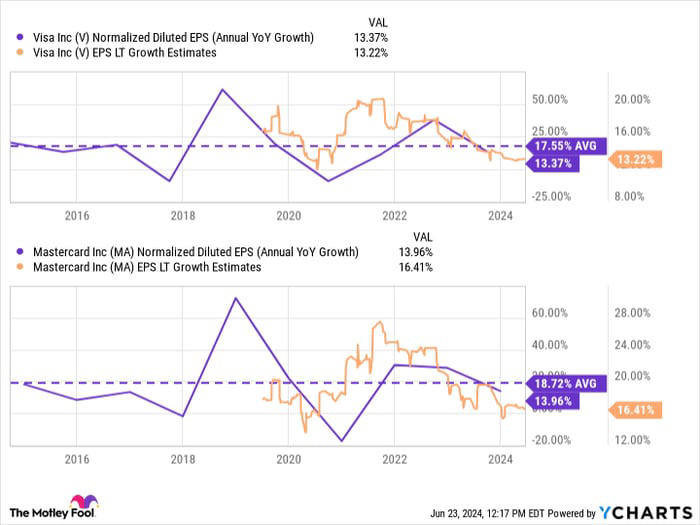

Right now, analysts are calling for long-term earnings growth for both companies that are slightly below their average over the past 10 years:

V Normalized Diluted EPS (Annual YOY Growth)

Estimates should be taken with a grain of salt because they can change as circumstances change, but it's wise to be cautious when dealing with any stock carrying a high valuation. Notably, the long-term growth prospects look strong for both companies because the massive shift away from cash still has room to run.

According to research by Consultancy.UK, non-cash transactions are growing by an average of 15% annually through 2027. Additionally, Visa and Mastercard's fees are percentage-based, which makes them benefactors if continued inflation drives up transaction values. That should mean the wind remains in Visa and Mastercard's sails for the foreseeable future.

Here is the game plan

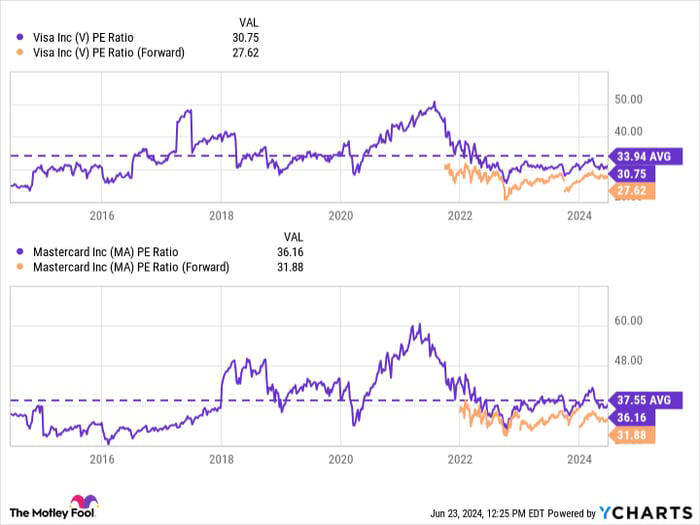

Investors who are worried about Visa and Mastercard's size -- an understandable concern at this point -- should avoid chasing the stock at nosebleed valuations. Fortunately, both stocks seemingly trade at fair valuations today:

V PE Ratio

Using forward P/E ratios since we are halfway through the year, both stocks are notably below their decade-long averages. One could argue that such discounts compensate investors for the risk of slowing growth due to their size.

The same tailwinds that have driven years of profitable growth and robust investment returns remain. Given each stock's history, its reasonable price tags make it a no-brainer buy today.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Amazon: if you invested $1,000 when we doubled down in 2010, you’d have $21,805!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $40,295!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $365,472!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, and there may not be another chance like this anytime soon.

See 3 “Double Down” stocks »

*Stock Advisor returns as of June 24, 2024

Justin Pope has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Mastercard and Visa. The Motley Fool recommends the following options: long January 2025 $370 calls on Mastercard and short January 2025 $380 calls on Mastercard. The Motley Fool has a disclosure policy.