Brokers Digest: Local Equities - ITMAX System Bhd, Kimlun Corp Bhd, IHH Healthcare Bhd, Datasonic Group Bhd

This article first appeared in Capital, The Edge Malaysia Weekly on June 10, 2024 - June 16, 2024

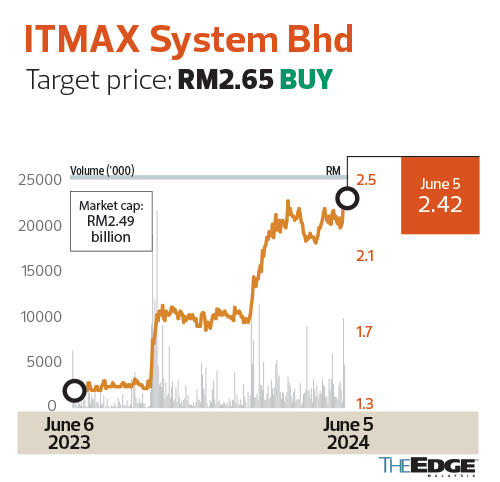

ITMAX System Bhd

Target price: RM2.65 BUY

MAYBANK INVESTMENT BANK GROUP RESEARCH (JUNE 5): ITMAX (KL:ITMAX) has secured its maiden Letter of Award (LoA) for smart parking operations in Johor, in effect creating a new revenue vertical for the group.

ITMAX’s 65%-subsidiary, Southmax Sdn Bhd (SSB) was awarded a LoA by Majlis Bandaraya Iskandar Puteri (MBIP), appointing it as the smart parking operator for 32,025 street parking bays in Bandar Iskandar Puteri. The LoA is for a period of 15 years until May 31, 2039. This is ITMAX’s first smart parking contract following its acquisition of 70% equity interest in Aim-Force Software for RM7.2 million in August 2023.

Per the terms of the LoA, SSB will be fully responsible for the management and maintenance of the smart parking system in the district. Revenue generated from operations will be split between SSB and MBIP in a 70:30 ratio, with the revenue-share model applied to all cash proceeds collected via SSB’s parking app, Parkmax@Johor. To note, MBIP successfully trialled SSB’s app in Bandar Iskandar Puteri from April 1 to April 30, 2024 and intends to fully digitise parking in the district by Jan 1, 2025.

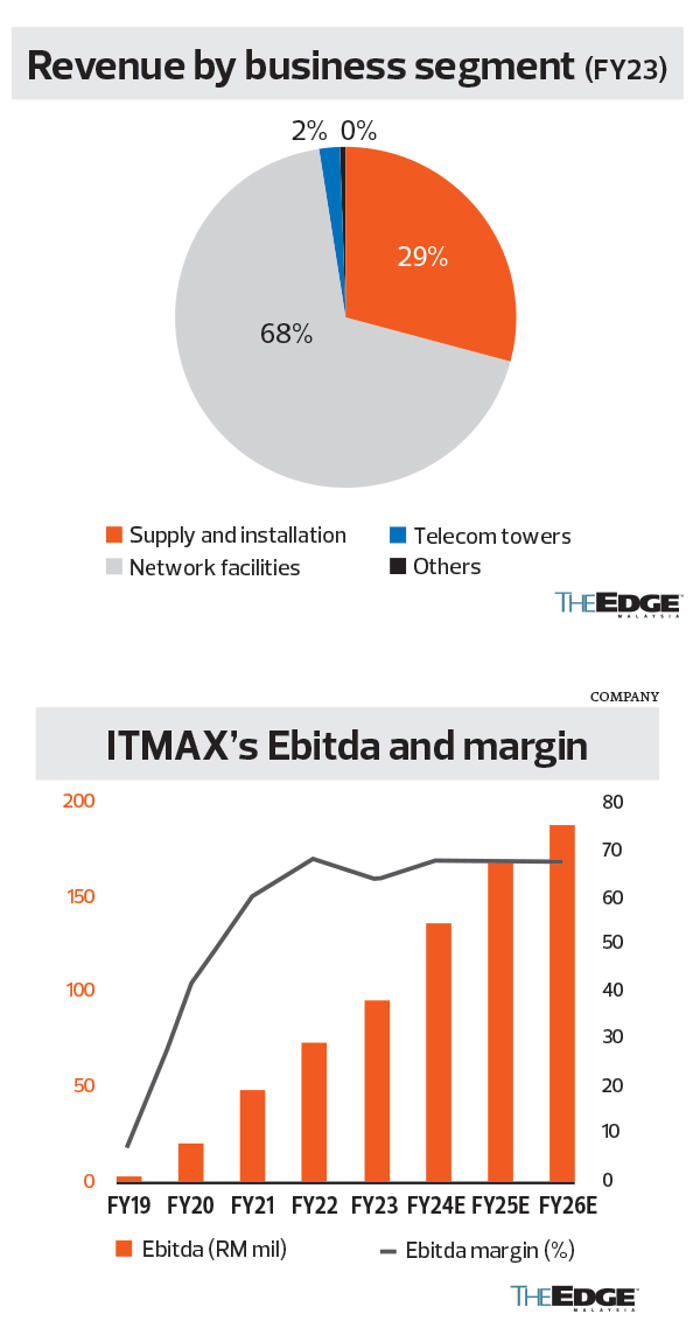

We estimate that every incremental 10,000 parking bays assigned to SSB have the potential to accrete RM4.1 million a year to ITMAX’s turnover and RM1.4 million to Patami.

In addition to MBIP’s 32,000 street parking bays, there are roughly 90,000 parking bays under the purview of Majlis Bandaraya Johor Bahru and a further 30,000 each under Majlis Bandaraya Pasir Gudang and Majlis Perbandaran Kulai — ITMAX has subsisting CCTV contracts with all four district councils. We believe that the usage of SSB’s Parkmax app is highly scalable across other districts in Johor (subject to SSB being granted LoAs first by the respective district councils) due to its user-friendly user interface and user experience.

Having previously imputed for parking revenue of RM7.4 million/RM11 million/RM14.7 million in FY24-FY26E, we maintain our earnings forecasts and target price of RM2.65 (pegged to 1.5 times price-earnings-to-growth ratio).

Maintain “buy” on compelling long-term outlook as ITMAX rides the tailwinds of Johor’s economic growth.

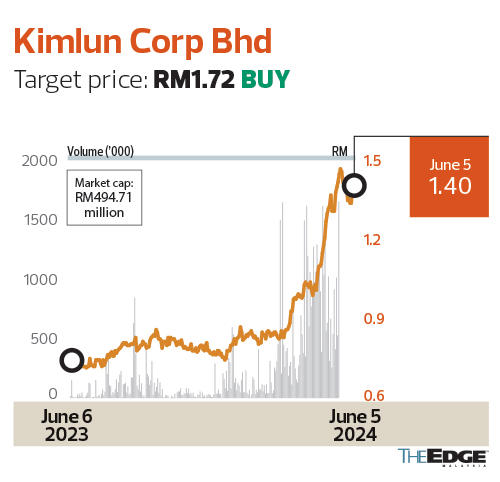

Kimlun Corp Bhd

Target price: RM1.72 BUY

HONG LEONG INVESTMENT BANK RESEARCH (JUNE 5): Kimlun (KL:KIMLUN) announced a contract win worth RM234.3 million from Saujana Development Sdn Bhd in relation to a high-rise residential development, representing its third construction contract win since March 2024. This takes its construction win year to date to RM1.05 billion. With this, our estimate of unbilled construction order book rises to RM2.8 billion (sizeable 4.4 times cover on FY23 construction revenue).

The precast division’s order book of RM370 million is also at a healthy level. The company should comfortably secure RM200 million of new precast orders with upside risk from higher demand for industrialised building system components, data centres, impending infra upcycle in Singapore and mega projects rollout in Malaysia. Kimlun’s timely capacity expansion is expected to be commissioned and will commence operations in September this year.

Total unbilled orders now stand at RM3.16 billion. Based on its tender book of RM2 billion, we now see upside risks to our newly revised construction win assumption. Maintain “buy” with unchanged target price of RM1.72, pegged to 11 times PER, a 40% discount to the KL Construction Index.

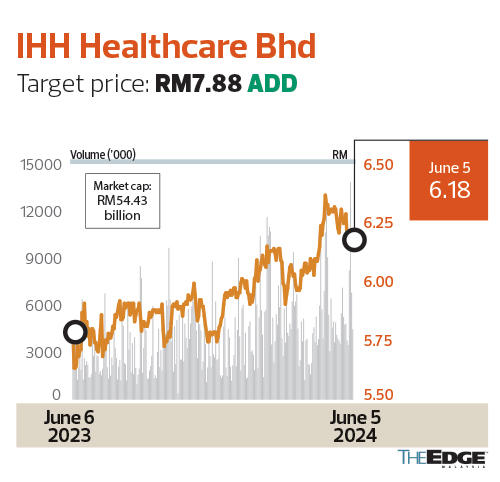

IHH Healthcare Bhd

Target price: RM7.88 ADD

CGS INTERNATIONAL RESEARCH (JUNE 4): IHH (KL:IHH)’s 1Q24 core net profit (ex-MFRS129) of RM586.4 million was ahead of expectations, at 28.1% of our and 32.9% of Bloomberg consensus FY24 estimates. An increase in revenue intensity across all key operating regions supported the record revenue of RM5.96 billion in 1Q24, translating into improved Ebitda margin.

All key operating business units recorded y-o-y revenue growth to support Ebitda growth, except Malaysia (4% decline on an initiative to reward healthcare workers). Revenue growth was predominantly driven by double-digit growth in revenue per inpatient y-o-y across key regions (Malaysia +10%; Singapore +15%; Turkey and Europe +51%; and India +11%) while total inpatient admissions were relatively stable.

Maintain estimates and our “add” call (with an unchanged SOP target price of RM7.88) as we are positive on various levers of growth across its operating regions. Rerating catalysts include better communication of impact from MFRS129 on core underlying performance that excludes hyperinflationary environment in Turkey, sustained improvement in Ebitda margins for India and Turkey and Europe, as well as an accelerated increase in bed capacities to support higher inpatient volumes.

Datasonic Group Bhd

Target price: 68 sen BUY

RHB RESEARCH (JUNE 5): Datasonic (KL:DSONIC) accepted Letters of Extension worth RM182 million from the Ministry of Home Affairs for the supply of national identity (ID) cards, comprehensive maintenance services, and e-Passports solutions for another six months ending Nov 30, 2024. The contract extensions are within expectations and should help to boost investor confidence in its capabilities in delivering mission critical projects with great value and without disruption.

Following the contract extensions, the group’s order book stands at around RM280 million. Management remains committed to securing the long-term contracts for both ID card and passport solutions, along with the new hardware and printing systems, autogate solutions, and identity management system. The group is also working on a new solution with artificial intelligence features to improve clearance time for the MBike system at Johor Bahru’s border control.

We maintain our forecasts as the contract extensions are within expectations. Target price remains at 68 sen, based on an unchanged 20 times FY25F PER. We like Datasonic for its competitive strength in its niche solutions, healthy yields, strong cash flow generation and potential upside from new project wins.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's App Store and Android's Google Play.