Why Sandeep Bakhshi's exit from ICICI Bank may knock-off the Street

ICICI Bank’s prompt denial of Managing Director Sandeep Bakhshi “sending feelers” about his desire to exit as reported by The Morning Context managed to arrest any significant erosion in the stock in today’s trade. The ICICI bank stock ended 1 percent lower at Rs 1,139 per share on May 2.

But analysts said it’s not difficult to see why any such news would send a big shock to markets and prove to be sentimentally-negative for ICICI Bank.

From Rs 355 per share in October 2018 to smooth sailing at Rs 1,152 currently, ICICI Bank’s four-fold jump in stock price reflects investors’ faith in the private lender ever since Sandeep Bakhshi donned the heavy hat from Chandra Kochhar. It’s under his leadership that the bank outpaced SBI, the largest bank in the country by size, in terms m-cap.

The big transition

Sandeep Bakhshi’s step-up in ICICI Bank came at a time when the lender was not in the best of its shape on October 15, 2018. Prior to his appointment as MD and CEO of ICICI Bank, he was a whole-time director and chief operating officer of the bank. The change of baton took place when predecessor Chandra Kochhar was forced out due to money laundering allegations, wavering investors’ confidence to a low. But Bakhshi took ICICI Bank from third-largest lender in India by m-cap to second-largest (next only to HDFC Bank).

ICICI Bank’s m-cap rose to Rs 8.09 lakh crore in 2024 from Rs 2.01 lakh crore in 2018, outpacing State Bank of India’s Rs 7.36 lakh crore m-cap, showed data from Bloomberg. Stock also saw a stellar rally, giving over 200 percent returns in the span of 6 years.

lovisha_may2 (2)

“Bakhshi has done a wonderful job in the last six years. He has revamped retail lending, deepened bank’s reach across geographies, improved profitability, and brought down bad loans,” said Jignesh Shial, Director – Research and Head of BFSI Sector at InCred Capital.

Dnyanada Vaidya, BFSI Research Analyst at Axis Securities also agreed. She said the since 2018 ICICI Bank’s risk-reward metrics turned favourable and the bank has delivered an all-round performance across operational metrics consistently.

The three-fold jump

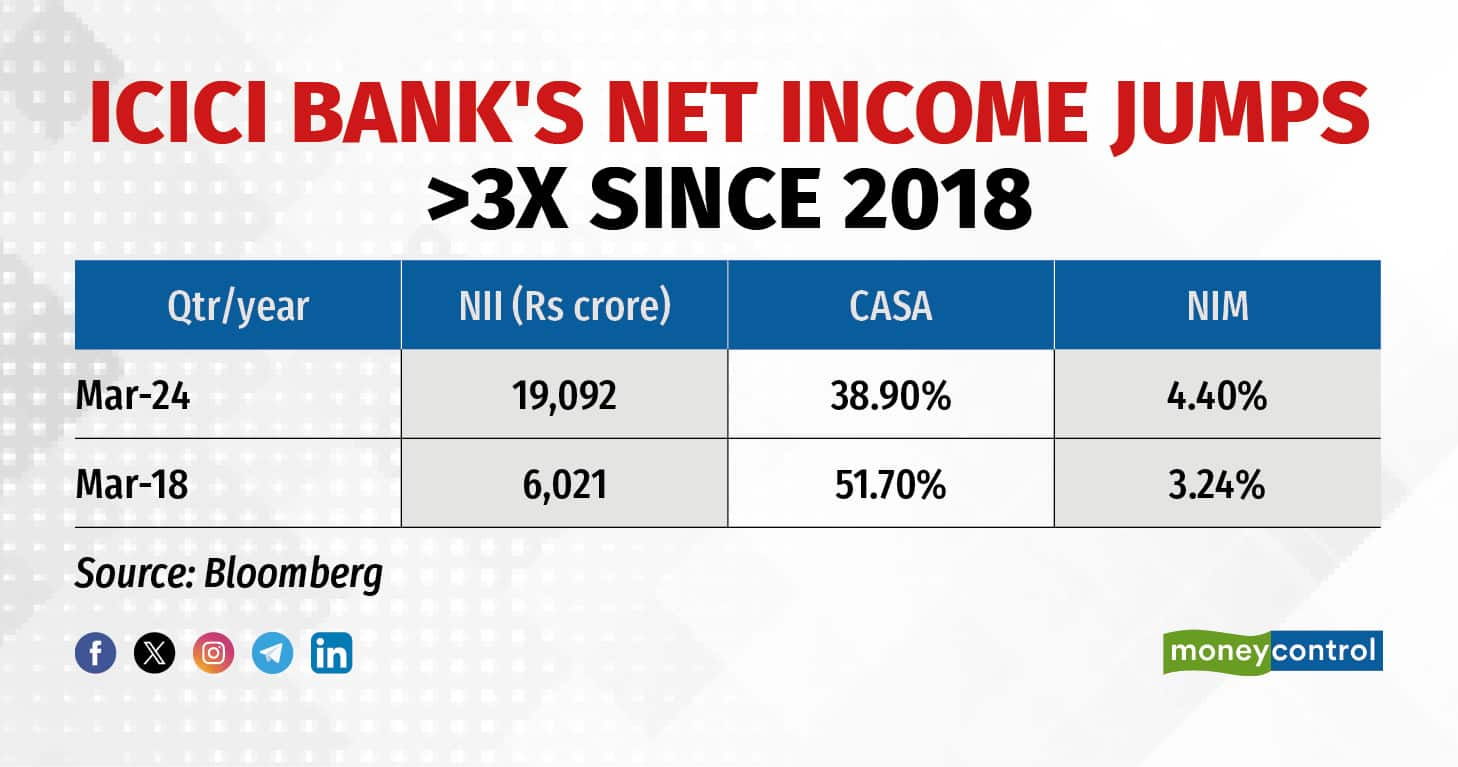

Besides, during his tenure, ICICI Bank’s bad loans saw a steep decline. The bank’s net non-performing assets (NNPAs) declined tremendously to 0.45 percent in the March-ended quarter of fiscal year 2023-24 (Q4FY24) from 5.43 percent in Q4FY18.

ICICI BANK

Additionally, the private-sector lender’s net interest income jumped over three-fold to Rs 19,092 crore in Q4FY24 from Rs 6,021 crore in Q4FY18, while margins expanded by 120 basis points to 4.4 percent in the last 6 years. Similarly, at 4.86 percent, ICICI Bank’s cost of funds were marginally lower than HDFC Bank’s 4.9 percent and way better than Axis Bank’s 5.4 percent.

The overhang in this picture perfect scenario remains deteriorating current and savings account (CASA) ratio. CASA ratio declined to 38.9 percent in Q4FY24 from 51.7 percent in Q4FY18. But analysts said that this situation was seen across industry as all CASA flows went to term deposits in a rising rate scenario.

Street upbeat on ICICI Bank

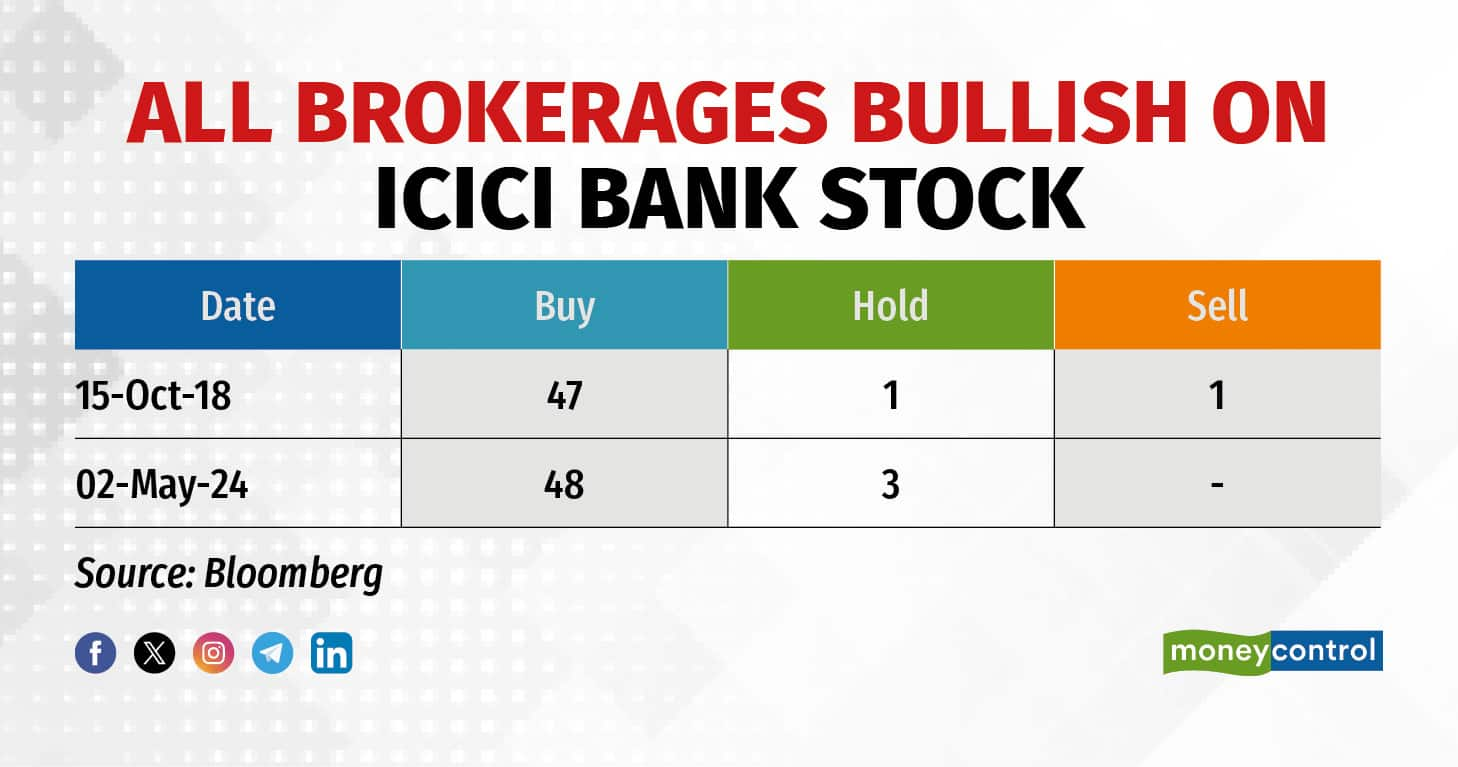

With Bakhshi managing to front the ship in smooth waters over the course of 6 years, all brokerages turned favourable on the stock. At present, there were zero ‘sell’ calls on ICICI Bank, while ‘buy’ calls stood at 48, and 3 were on ‘hold’, showed Bloomberg data.

ALL BROKERAGES BULLISH ON ICICI BANK STOCK

The lender’s return on equity (RoE) – which measures how effectively a company generates profit also jumped to 17.2x in 2023 from 5.24x in 2019.

Going ahead, Jefferies analysts see further scope of re-rating in ICICI Bank due to better growth prospects and attractive valuations against peers. “Since valuations are reasonable at 13x FY26, we upgrade FY25/26 EPS by 4 percent each,” they wrote in a recent note, sharing an ‘overweight’ rating and target price of Rs 1,300 apiece.

Nomura, too, expects the lender to deliver 13 percent profit-after-tax (PAT) compounded annual growth rate (CAGR) over FY24-26 after reporting a strong Q4FY24. The brokerage firm shared a ‘buy’ call with a target price of Rs 1,335 per share.

With the best quality private sector banks – HDFC Bank and Kotak Bank – struggling to perform on the bourses, analysts and fund managers have been increasingly leaning towards ICICI Bank. A leadership change, if it comes through, may leave fund managers with no easy options in the BFSI space.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.