Pension trap: Investors can rack up big losses early on and never make them up if they aren’t careful.

Pound cost ravaging is a nasty trap which can do severe damage to pension investments, especially in the early years of retirement.

It means that when markets fall you suffer the triple whammy of falling capital value of the fund, further depletion due to the income you are taking out, and a drop in future income.

In financial jargon, this is also known as negative pound cost averaging, or sequencing risk.

It poses a problem every time markets take a tumble, but is especially dangerous at the start of retirement because investors can rack up big losses and never make them up again if they aren’t careful.

On top of that, people who persist in taking an income in the initial years will crystallise their losses and pile up problems for the future.

Taking an income from shrinking investments early on can do disproportionate and irreparable harm to your portfolio, because it is much harder to rebuild it to a position of strength.

But you can put defences in place against market shocks before you retire, and there are ways to overcome investment setbacks in the early years too. Find out what strategies are open to you below.

How does pound cost ravaging work?

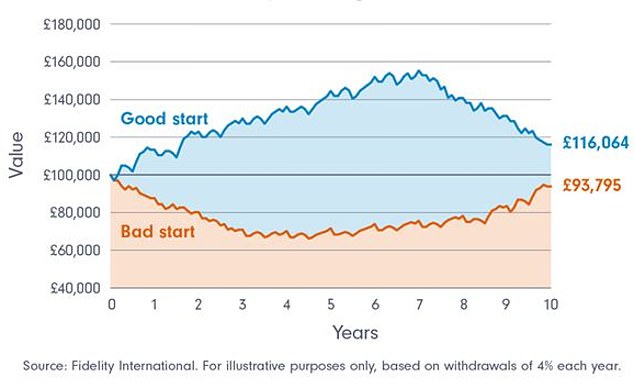

A financial market sell-off is worrying for anybody relying on pension investments to fund retirement income, but as outlined above it it can cause particularly big problems at the outset. The graph below illustrates what might happen.

‘Let’s say that over 10 years, your portfolio will earn an average annual return of 5 per cent,’ explains Ed Monk, associate director at Fidelity International.

‘Some years you’ll get higher returns. Some years they’ll be lower (perhaps even a loss). If you start to take an income when your investments are performing well, you won’t have to sell as many investments to get the income you need.

‘This will give you a “good start” to drawing an income and you can see this on the graph in blue (below). Even though your returns fall in later years, you’re still left with just around £116,064 in your pension pot.’

But Monk says if you start to draw down an income at a point when your investments aren’t doing very well, you will have to sell more investments.

‘This is the “bad start” shown by the orange line. By the time ten years have passed, your pot is significantly smaller than if you’d enjoyed the “good start”.’

‘This is why it’s important to evaluate how your investments are doing when you start to take an income from your pension pot.’

Monk says the two examples use exactly the same illustrative investment returns but in reverse order regarding the timing of the good and the bad years.

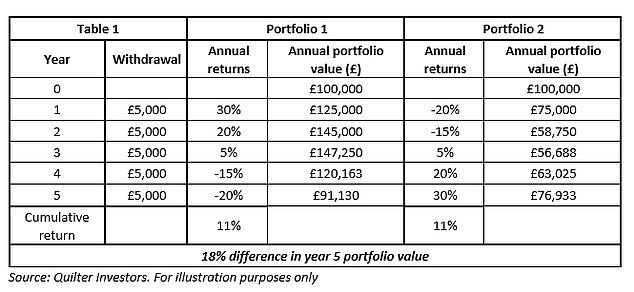

The table below from Quilter also highlights the impact of early losses versus early gains.

‘When you sell units for income you lock in these losses, making it harder for the portfolio’s value to fully rebound. This is despite the cumulative return without withdrawals being identical in both cases,’ says CJ Cowan, income portfolio manager at Quilter Investors.

‘In a market that trends upwards, selling units in a fund to generate income works just fine. But in a sideways, down trending, or particularly volatile market a different investment strategy is required.’

How do you protect yourself ahead of retirement?

It’s sensible to prepare in advance just in case of market trouble early on in your retirement.

You can avoid making withdrawals and crystallising losses on your pension investments if you have cash on hand, or other assets and sources of income to draw on instead while you wait until the market calms down.

Monk says: ‘By carving out a pot of cash savings and taking income from that in the first instance you can give invested money the chance to recover.

‘For example, hold two years’ worth of income as cash and pay yourself from that. After a year, if your invested money has fallen in value, you can take the second year of income from the cash pot rather than selling assets.

‘With luck, in the third year your investments will have recovered some ground and you can replenish your cash pot.’

What if the market crashes just after you retire?

There are a range of options to consider, depending on your personal circumstances, financial means and attitude to risk.

1. Use up your cash savings before selling investments

As mentioned above, you can prioritise spending your cash savings as a buffer against investment losses.

2. Take only ‘natural’ income from your investments

This means withdrawing only money generated from dividends in shares or funds of shares, or ‘coupons’ (the interest) from bonds.

‘By choosing a natural yield strategy, investors will likely see their portfolio tilted towards different asset classes, regions and sectors compared to a portfolio solely investing for long-term capital growth,’ says Cowan.

‘This will include sectors more associated with cheaper or “value” segments of the market.’

3. Review your pension investments

You might want to rethink your strategy, but that doesn’t necessarily mean moving into lower risk investments if you plan to stay invested throughout a retirement that could last decades.

If in doubt about how to build an investment drawdown portfolio, you should consider paying for financial advice.

4. Halt or vary the size of withdrawals if you can

Many people investing their pensions often don’t realise they can adjust or stop withdrawals, research has revealed in the past.

Some retirees need to keep taking a regular income from investments to cover immediate living expenses in old age, but if not you can consider a more ad hoc approach.

5. Delay your retirement plans

You can put off retirement if your personal circumstances allow this, or consider going back to work or taking a different kind of job.

Anyone choosing to wait usually benefits from more investment growth. They can afford bigger withdrawals and their savings are likely to last longer.

6. Consider alternatives to drawdown

Buying an annuity to fund retirement is an irrevocable decision, but you can change your mind about income drawdown, especially if you are getting on in years and feel less able to manage investments.

You can still opt to put all or some of your money into an annuity. You can consider combining drawdown and annuities to maximise retirement income. Interest rate rises have led to better annuity deals.

7. Be opportunistic and buy

This is risky, so only for the bravest, most experienced or wealthiest investors – those who can afford losses without damaging their standard of living.

But market dips can be the cheapest time to buy if you are looking to invest over the long haul.

News Related-

Up to 40 Tory MPs ‘set to rebel’ if Sunak’s Rwanda plan doesn’t override ECHR

-

Country diary: A tale of three churches

-

Sunak woos business elite with royal welcome – but they seek certainty

-

Neil Robertson shocked by bad results but has a plan to turn things round

-

Tottenham interested in move to sign “fearless” £20m defender in January

-

Bill payers to stump up cost of £100m water usage campaign

-

Soccer-Venue renamed 'Christine Sinclair Place' for Canada soccer great's final game

-

Phil Taylor makes his pick for 2024 World Darts Championship winner

-

Soccer-Howe aims to boost Newcastle's momentum in PSG clash

-

Hamilton heads for hibernation with a word of warning

-

Carolina Panthers fire head coach Frank Reich after 1-10 start to the season

-

This exercise is critical for golfers. 4 tips to doing it right

-

One in three households with children 'will struggle to afford Christmas'

-

Biden apologised to Palestinian-Americans for questioning Gaza death toll, says report